Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A financing technique that leverages the same asset as collateral to secure multiple loans

Cross-collateralization occurs whenever a borrower pledges one asset to serve as collateral to secure multiple loans, enhancing the appeal for lenders. Although the default risk may be lower if the lender deems the existing collateral stronger than other security associated with the new debt, defaulting on any loan may be an automatic default on all loans (i.e., a form of cross-default).

Compliance with all terms (e.g., payments as agreed and adherence to covenants) for all loans that use the same collateral is paramount. If not, the lender can take enforcement action to realize its security, liquidate the collateral, and repay all loans that rely on the asset.

For example, real estate loans (e.g., mortgage, home equity line, etc.) are often cross-collateralized using the same property. If there are multiple lenders, a cross-default clause can also treat the default of loans to other lenders as a default on its loan since the same collateral is involved.

Beyond real property, any business asset or collateral can be cross-collateralized to multiple business loans. A typical financing technique for commercial lenders is a financing clause that all security of the borrower is collateral for all business debts.

Cross-collateralization is a versatile financing technique to secure various retail or commercial lending products. If the same lender is involved, the initial cost to pledge an asset is already paid, so using the collateral for multiple loans may be less costly.

Tangible assets with equity, such as real estate, automobiles, and other equipment, have greater appeal for cross-collateralization due to the surplus value available after the existing debt is settled.

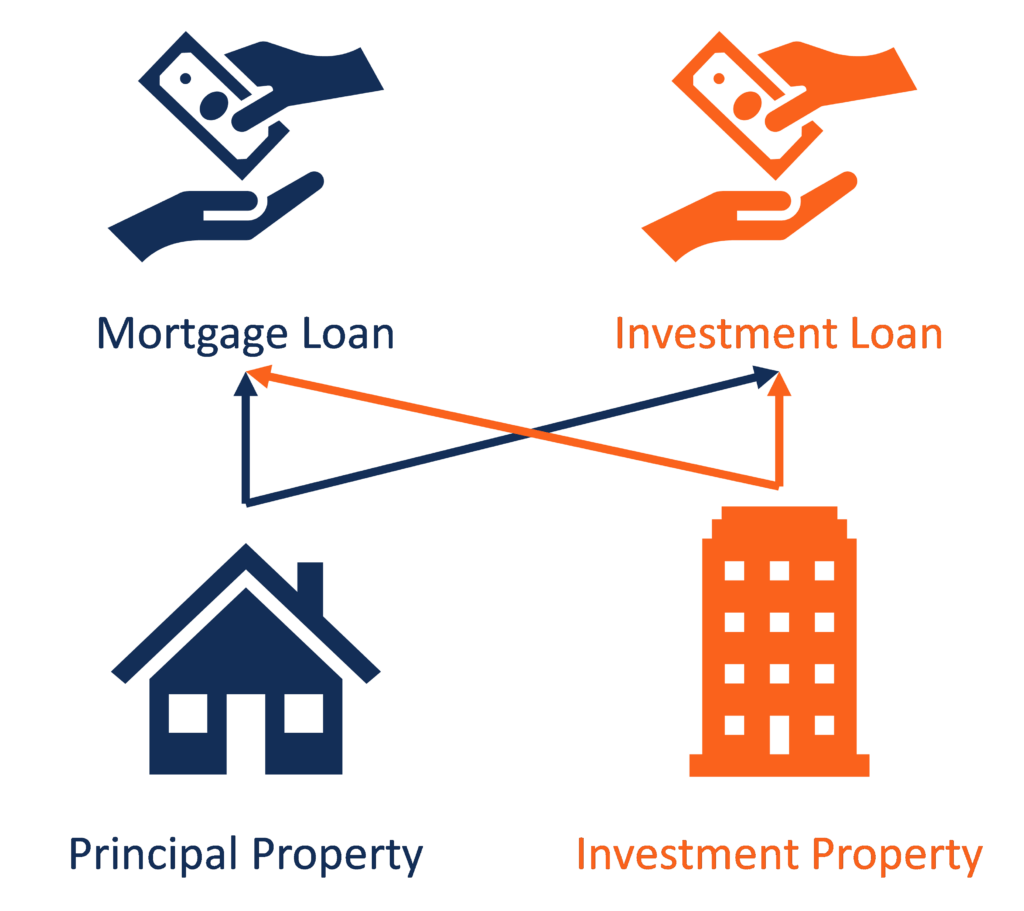

For example, a mortgaged property can cross-collateralize and secure an investment loan to purchase another property. The lender may lend strictly due to the equity of the original property, or use both properties as collateral for both loans. Circumstances may dictate the investment property is restricted for use as collateral, for example, a foreign property that cannot be secured.

General business and intangible assets, in the form of enterprise value, may backstop the value of a corporate guarantee signed by a stronger borrower in favor of a weaker borrower.

For example, an established corporate borrower creates a startup venture. The corporate borrower may offer cross-collateralization to the venture. The collateral supports the venture’s financing requirements until it can refinance on a standalone basis.

Some benefits to cross-collateralization:

While there are benefits, there are risks that come with using cross-collateralization:

Thank you for reading CFI’s guide on Cross-Collateralization. To keep learning and advancing your career, the additional CFI resources below will be helpful: