Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The entire value of a firm

Enterprise Value (EV) is the measure of a company’s total value. It looks at the entire market value rather than just the equity value, so all ownership interests and asset claims from both debt and equity are included. EV can be thought of as the effective cost of buying a company or the theoretical price of a target company (before a takeover premium is considered).

The simple formula for enterprise value is:

EV = Market Capitalization + Market Value of Debt – Cash and Equivalents

The extended formula is:

EV = Common Shares + Preferred Shares + Market Value of Debt + Noncontrolling Interest – Cash and Equivalents

Image from CFI’s free Introduction to Corporate Finance Course.

The value of the company can be derived from the assets it owns. However, obtaining the market value of each and every asset can be quite tedious and difficult. What we could do instead is look at how the assets have been paid for.

The simple accounting equation can serve as a guide by looking at assets as the application of funds and both liabilities and shareholder’s equity as the sources of funds used to finance those assets. When we say value, we mean the current or market value of the company, so it’s the market value of liabilities and the market value of equity that we consider.

Equity value is found by taking the company’s fully-diluted shares outstanding and multiplying it by a stock’s current market price. Fully diluted means that it includes in-the-money options, warrants, and convertible securities, aside from just the basic shares outstanding.

If a company plans to acquire another company, it will need to pay that company’s shareholders by paying at least the market capitalization value. This alone is not considered an accurate measure of a company’s true value, and for that reason, other items are added to it as seen in the EV equation.

Total debt is the contribution of banks and other creditors. They are interest-bearing liabilities and are comprised of short-term and long-term debt. The amount of debt gets adjusted by subtracting cash from it because, in theory, when a company has been acquired, the acquirer can use the target company’s cash to pay a portion of the assumed debt. If the market value of debt is unknown, the book value of debt can be used instead.

Preferred stocks are hybrid securities that have features of both equity and debt. They are treated more as debt, in this case, because they pay a fixed amount of dividends and have a higher priority in asset and earning claims than common stock. In an acquisition, they normally must be repaid just like debt.

Noncontrolling interest is the portion of a subsidiary not owned by the parent company (who owns a greater than 50% but less than 100% position in the subsidiary). The financial statements of this subsidiary are consolidated in the financial results of the parent company.

We add this noncontrolling interest to the calculation of EV because the parent company has consolidated financial statements with that noncontrolling interest; meaning the parent includes 100% of the revenues, expenses, and cash flow in its numbers even though it doesn’t own 100% of the business.

By including the noncontrolling interest, the total value of the subsidiary is reflected in EV.

Learn more about minority interest in enterprise value calculations.

This is the most liquid asset in a company’s statement. Examples of cash equivalents are short-term investments, marketable securities, commercial paper, and money market funds. We subtract this amount from EV because it will reduce the acquiring costs of the target company. It is assumed that the acquirer will use the cash immediately to pay off a portion of the theoretical takeover price. Specifically, it would be immediately used to pay a dividend or buy back debt.

Enterprise Value is often used for multiples such as EV/EBITDA, EV/EBIT, EV/FCF, or EV/Sales for comparable analysis such as trading comps. Other formulas, such as the P/E ratio, usually don’t take cash and debt into account like EV does. Hence, two identical companies that have the same market cap may have two different enterprise values.

For instance, Company A has $60 million in market cap, $20 million in cash, and carries no debt. Company B, on the other hand, also has $60 million in market cap, but has no cash, and carries $30 million of debt. In this simple scenario, we can see that Company A is cheaper to buy because it doesn’t have any debt to pay off creditors.

Enterprise Value is very useful in Mergers and Acquisition situations, especially with controlling ownership interests. In addition, it is useful for comparing companies with different capital structures because a change in capital structure will affect the amount of enterprise value.

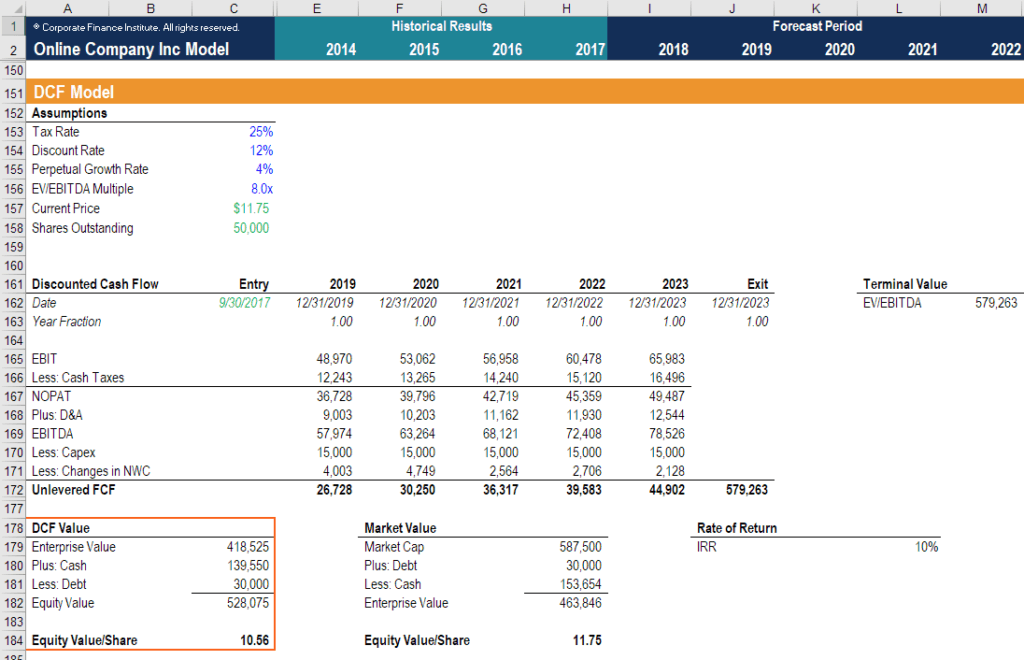

In financial modeling, it is common practice to model Free Cash Flow to Firm (FCFF), which is based on the cash flow derived from 100% ownership of all assets and, therefore, determines a company’s Enterprise Value.

As you can see in the example above, row 172 produces Unlevered Free Cash Flow (the same thing as FCFF). From there, the XNPV function is used to calculate Net Present Value, which is the EV in cell C197.

The above screenshot was taken from CFI’s financial modeling courses.

Thank you for reading CFI’s guide to Enterprise Value. To continue advancing your career, these additional resources will be helpful: