Secured vs Unsecured Loans

Learn about the different types of loans

What are Secured vs Unsecured Loans?

When planning to take out a personal loan, a borrower can choose between secured vs unsecured loans. When borrowing money from a bank, credit union, or other financial institution, an individual is essentially taking a loan. The bank has the discretion to decide whether to require the borrower to provide an asset as collateral for the loan (secured loan) or extend the loan without any preconditions (unsecured loan).

The collateral serves as a security for the loan. Collateral can be a motor vehicle, real estate property, or other assets that the borrower provides as a security for the loan. If the borrower defaults on the agreed loan payments, the lender can sell or auction the collateral to recover the losses incurred.

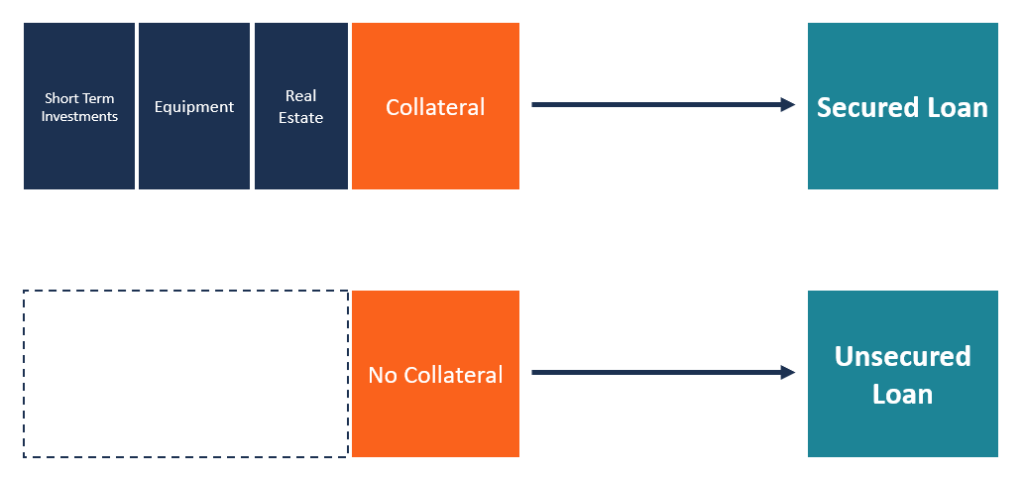

Summary

- Personal loans can be either secured or unsecured, depending on whether or not the lender requires borrowers to pledge a property or other asset as collateral.

- A secured loan is secured by collateral, which can either be a motor vehicle, house, savings account, certificate of deposit, etc.

- An unsecured loan is not backed by collateral, and it is only based on the borrower’s creditworthiness and the ability to make timely loan repayments.

What are Secured Loans?

A secured loan is a type of loan where the lender requires the borrower to put up certain assets as a surety for the loan. In most cases, the asset pledged is usually tied to the type of loan that the borrower has applied. For example, if the borrower has requested for an auto loan, the collateral for the loan would be the motor vehicle to be financed using the loan amount.

Similarly, if the borrower takes a mortgage to buy a house, the purchased house is put up as a surety for the loan until the loan has been fully paid. If the borrower delays or defaults on the loan, the lender has the right to seize the property or other pledged assets to recover the outstanding balance of the loan.

When extending a secured loan to the borrower, the lender requires the asset to be properly maintained and insured. For mortgages and auto loans, the lender may require the borrower to take out a specific type of insurance that protects the worth of the asset. Lenders with an internal insurance department or preferred insurers may require borrowers to insure with them or with the recommended insurers to protect their interests. Getting the asset insured with the proper coverage ensures that, in case of an accident, fire, or natural disasters, the lender can recover the outstanding balance of the loan from the insurance payments.

What are Unsecured Loans?

An unsecured loan is a loan that does not require collateral, and the loan is not tied up to any asset. When providing an unsecured loan, the lender relies on the creditworthiness of the borrower and their guarantee to pay back the loan as per the agreement. Due to the high risk associated with unsecured loans, banks practice a lot of caution when evaluating the creditworthiness of a borrower. Lenders are only interested in lending to the most credible borrowers who have some history of making timely payments, clean credit history with other lenders, and strong cash flow.

Since unsecured loans are not backed by assets, they carry a relatively higher level of risk than asset-backed secured loans. To compensate for the added risk, lenders charge a higher interest rate than secured loan lenders. Without collateral, the lender has a greater liability of losing the outstanding balance of the loan.

However, some unsecured loans, such as Treasury bills, do not come with high interest rates despite not having collateral. Even though investors do not have a claim on the government’s assets, they bank on the government’s ability to collect revenues through taxes.

Secured vs Unsecured Loan Lenders

The most common types of lenders for personal loans include banks, credit unions, and online lenders. Such lenders offer both secured and unsecured loans and impose varying loan-qualification requirements. Banks put out more rigorous requirements. They require borrowers to provide collateral when applying for specific types of loans such as auto loans, equipment loans, working capital loans, mortgage, etc.

Credit unions impose less rigid requirements for loans. Borrowers must be members of the union in order to qualify for credit facilities. For low amounts of loan, both banks and credit unions may consider the credit score of an individual, without requiring them to provide specific assets as collateral.

However, for specific types of loans such as mortgages and auto loans, lenders may require borrowers to provide proof of employment and business cash flows. On the other hand, borrowers pledge the asset being financed as collateral. Online lenders mainly offer unsecured loans, since they mainly lend small amounts of loan. The borrowers must demonstrate a positive credit history and high credit score in order for their loan requests to be approved.

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: