Get Certified for

Financial Planning & Wealth Management Professional (FPWMP™)

Learn financial analysis & planning, portfolio management, and risk assessment.

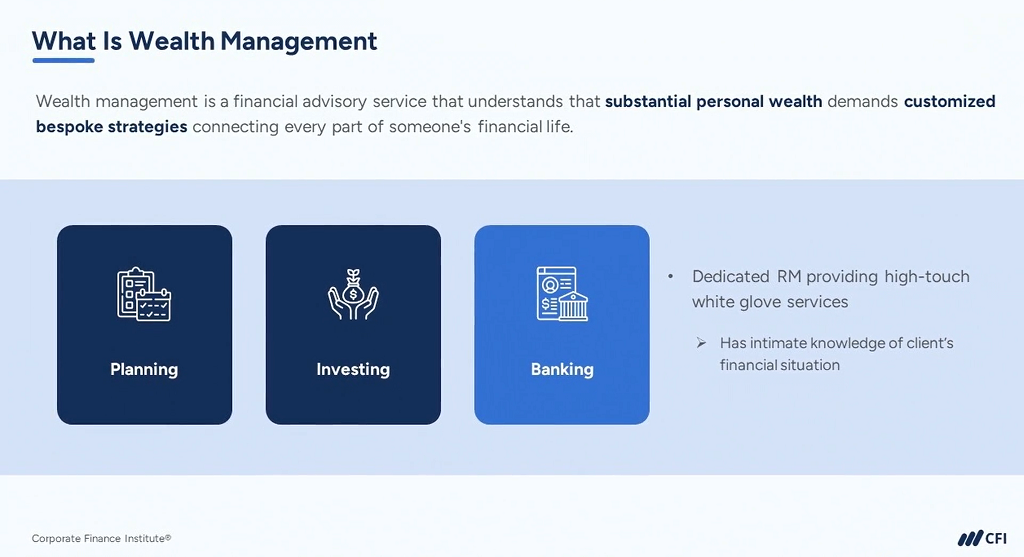

Wealth management is a holistic financial advisory service that focuses on protecting and growing the wealth of high and ultra-high-net-worth clients. In other words, wealth management provides a wide array of financial advice to wealthy individuals to help them make smart financial decisions that will help them both maintain and increase their wealth.

Wealth managers develop a strategy to maintain and increase their clients’ wealth based on each client’s financial situation, goals, and risk tolerance. Each component of a wealth management strategy must also protect the wealth of the clients in some way.

Once a wealth manager develops a client’s main financial advisory plan, the wealth manager will regularly meet with the client to update goals and review the client’s financial portfolio based on possible risks and new financial opportunities. The wealth manager will also review the client’s financial portfolio to rebalance it. During regular wealth management meetings, wealth managers will even investigate if the client would benefit from additional financial services.

It’s important to note that wealth managers should always be conscious of their clients’ risk tolerance, as ignoring a client’s financial risk tolerance due to current life situations could cause the client to lose money and not achieve his or her goals.

For example, if a client is getting close to retiring and thus needs to save as much money as possible to maintain a lifestyle in retirement, a wealth manager should recognize that the client’s risk tolerance is decreasing. Therefore, the wealth manager should suggest much safer investments than before.

Because wealth management is a holistic financial advisory service, it creates financial plans for clients that incorporate all aspects of their lives. Thus, wealth management focuses on a wide range of services from accounting and tax services to investment advice, to estate planning, and helping clients save for retirement. A full list of financial advisory services that wealth managers offer is available below.

There are numerous reasons why wealth management is beneficial. One is that wealth management helps mitigate financially draining sources such as taxes and fees. Wealth management also specializes in managing a person’s investments and growing a person’s wealth while minimizing risk. Furthermore, wealth management can help clients maintain adequate insurance in all forms, saving individuals from paying egregious out-of-pocket bills.

While wealth management helps affluent people save money, it also indirectly helps them to give back money to less fortunate people. This is because wealth management helps affluent people pass their wealth down to their loved ones and other beneficiaries through legacy and estate planning. Wealth management also helps to maximize the reach and impact of charitable giving by affluent people.

Another major benefit of wealth management is that it provides its clients with holistic financial guidance. As a result, all aspects of a client’s financial life, from taxes to retirement funds, get addressed and taken care of when receiving wealth management services. Furthermore, wealth management clients receive this holistic financial guidance from wealth managers who are experts in their field.

While wealth management is holistic, it’s also very personalized. Thus, each individual client contains a different financial plan that is specific to his or her financial situation, goals, and risk tolerance. By providing clients with such individualized care, wealth managers help their clients maximize their returns.

Arguably, one of the biggest benefits of wealth management is the time it saves clients from having to manage their finances themselves. On top of the peace of mind that wealth management provides its clients with terms of long-term financial security, the time saved on managing finances makes it a highly coveted financial advisory service.

As mentioned at the top of this article, wealth management is specifically for individuals with high or ultra-high net worths. The U.S. Securities and Exchange Commission (SEC) defines high-net-worth people as individuals with at least $750,000 in assets under management (AUM), or a net worth of $1.5 million or more. Wealth managers usually require individuals to have a certain amount of investable assets to be clients. Wealth managers’ minimum required amount of client investable assets ranges from $5,000 to $1 million.

Wealth managers can charge for their services in a number of ways. They can work for fee-only and charge an annual, hourly, or flat rate fee. They can also charge through commission based on the investments they sell. Fee-based advisors typically earn a combination of a fee plus some commissions on the investment products they sell.

It may be wise to get a wealth manager that works with a fee-only fiduciary, and thus can’t receive compensation for recommending certain products. Having a fiduciary duty legally obligates wealth managers to put the needs of their clients before their own. Like most financial advisors, wealth managers typically charge clients an annual set fee. This fee is usually a percentage of the client’s overall assets under management (AUM).

A standard annual fee rate for a wealth manager is 1% of a client’s annual AUM. For example, a person with an AUM of $1 million who has a wealth manager who charges an annual fee of 1% of the client’s AUM, will have to pay the wealth manager a $10,000 yearly fee.

Note that clients with higher AUMs tend to have lower fee rates. It’s also important to note that even if a wealth manager charges a set percentage fee of AUM, a client may pay more than that. This is because percentage fees don’t account for the underlying expenses associated with brokerage services, funds, and trading. The only exception is if the wealth manager uses a wrap-free program that bundles all expenses in a singular, annual rate.

While all wealth managers are financial advisors, not all financial advisors are wealth managers. This is because a wealth manager is a specific type of financial advisor that caters solely to clients of high or ultra-high net worth. This is as opposed to regular financial advisors that cater to people of all income levels.

While wealth managers are more specific than regular financial advisors regarding the clientele they cater to, regular financial advisors are more specific regarding their services. This is because financial advisors advise clients on how to meet individual, short-term financial goals.

On the other hand, wealth managers provide a more holistic approach to financial advisory in that they create financial plans for their clients that incorporate all aspects of their lives. Thus, the financial plan that a wealth manager creates for a client can include everything from tax planning to estate planning, to advice on the client’s charitable/philanthropic giving, to retirement planning, and more.

One specific form of financial planning that wealth managers often cover that regular financial advisors don’t is investment planning. This is partly because high or ultra-high-net-worth clients will likely make larger and more frequent investments than those with lower to moderate-level incomes.

Examples of certifications that wealth managers often have are the Certified Wealth Manager (CWM) certification and the Chartered Financial Analyst (CFA) designation. An example of a certification that regular financial advisors often have is the Certified Financial Planner (CFP) certification.

While wealth managers often provide their clients with investment planning services, investment planning is just one of many financial planning services that wealth managers offer. This is because wealth management is a holistic form of financial advising. Thus, wealth managers look at each client’s overall financial picture and then provide them with the financial planning services they need to achieve their financial goals and improve their long-term financial well-being.

The financial planning services that a wealth manager may offer a client could be some combination of investment planning, tax planning, retirement planning, legacy planning, etc. On the other hand, asset planning focuses solely on providing clients with the best investments to allocate in their portfolios and preserve and grow their assets.

While certifications such as the Certified Wealth Manager (CWM) certification and the Chartered Financial Analyst (CFA) designation are more specific to the duties of a wealth management financial advisor, a wealth manager may contain additional financial advisory certifications. For example, the Certified Financial Planner (CFP) certification and the Personal Financial Specialist credential on top of the CFA designation are the top three professional advisor credentials.

The CFP credential is particularly beneficial for a wealth manager because it’s the most rigorous certification for financial planning. Individuals with CFPs are also held to a fiduciary standard and thus must put the interests of their clients above their own.

Certified public accountants (CPAs) are also beneficial in wealth management as they can best help with tax planning. Many wealth advisory firms contain both CFPs and CPAs on staff.

Individuals who don’t quite fit the profile of a wealth management client but still want to take advantage of the vast array of financial planning services that wealth managers offer should pursue alternatives to wealth management. Some alternatives to wealth management include the following:

Some online financial advisors offer portfolio/investment management and in-depth financial planning services from human financial planners. Thus, clients can work directly with online financial advisors to build holistic financial plans or reach specific goals. Because these financial advisory services are online, individuals must receive these services by phone or video conference.

Robo-advisors are automated platforms that use algorithms for portfolio/investment management based on risk tolerance and goals. One benefit of using robo-advisors for financial advisory needs is that it’s less expensive than wealth management. Just note that when using a robo-advisor, one may be unable to converse with a human.

Ultra-high net-worth individuals who want an alternative to wealth management can take advantage of family offices. Family financial advisory offices offer a more personalized approach to wealth management.

High-income earners can also opt for tax-optimizing investing platforms. Tax-optimizing investing platforms will ensure clients receive the highest returns when maxing out their tax-advantaged accounts. An example of a tax-optimized investing platform is Playbook.

Playbook provides both automated investing and financial advice for client bank accounts. Playbook also provides the earnings and tax opportunities people often miss out on for their bank accounts.

Another alternative to wealth management services is financial planning and budgeting apps. Some financial planning and budgeting apps allow people to connect the apps to their bank accounts to monitor their finances and spending and more easily develop a budget.

Connecting to the financial planning and budgeting apps will also allow individuals to track their account balances, transactions, investments, and financial progress. Some examples of financial planning and budgeting apps include Monarch and Simplifi.

Some online trading and financial management platforms offer similar services to traditional wealth management firms but with financial advisors and lower investment minimums and fees. For example, the digital platform Empower is an online wealth manager that aligns more with traditional financial advisors. Thus, Empower customers get access to human financial advisors who can create portfolios based on their risk tolerance and financial goals. Empower offers three tiers of service based on account size, with different management fees and perks at each level.

Arguably, the best online trading platform for wealth management services is TradeStation. Because TradeStation is self-directed, it’s designed for self-directed traders and investors who want ample advanced charting, technical analysis tools and resources, and trade automation capabilities.

Chase customers looking for a self-directed, online trading experience can use J.P. Morgan Self-Directed Investing. J.P. Morgan Self-Directed Investing is an online trading platform with zero commissions and no account minimums. Chase customers who prefer an automated online trading experience can use J.P. Morgan Automated Investing.

An index fund is a security that mimcs a specific market index. Index funds are good alternatives to wealth management because they offer a low-cost and easy way to build a diversified portfolio. You can invest in an index fund through an exchange-traded fund (ETF) or index mutual fund.

When choosing a wealth manager, there are multiple factors that clients should consider. Some of these factors include the following:

To help individuals find a good wealth manager, use an online aggregator such as SmartAsset to search for wealth manager terms and compare them. With SmartAsset, you can take a short, online questionnaire to match you with different types of financial advisors in your area. Once you receive your matches, you can then review them and set up interviews with them to find a wealth manager that fits your needs and preferences.

If you’re aspiring to be a wealth manager, you need to learn wealth management. One way to do this is to enroll in online courses and certifications on wealth management. CFI contains many wealth management courses and certifications that aspiring wealth managers can use. For an introduction to financial planning and wealth management, enroll in the CFI Introduction to Financial Planning and Wealth Management: Industry and Careers course.

Institutional Asset Management Career Profile

Wealth Management vs Investment Banking: A Guide to Deciding Which Role is Right for You