Overview

Historical VaR for Market Risk Overview

“Historical VaR for Market Risk” will equip financial professionals with the skills needed to calculate Value at Risk (VaR) using the Historical method, a widely adopted approach by financial institutions. The course covers both equity and fixed-income securities, providing a comprehensive understanding of how past returns can be used to measure market risk. Learners will gain hands-on experience through Excel-based exercises, where they will build and analyze Historical VaR models using real-life data. The course also covers essential concepts such as Price VaR, Yield VaR, and duration, with practical demonstrations to solidify understanding. By the end of the course, participants will be able to apply these techniques confidently to various financial instruments, enhancing their ability to measure market risk.

Historical VaR for Market Risk Learning Objectives

Upon completing this course, you will be able to:

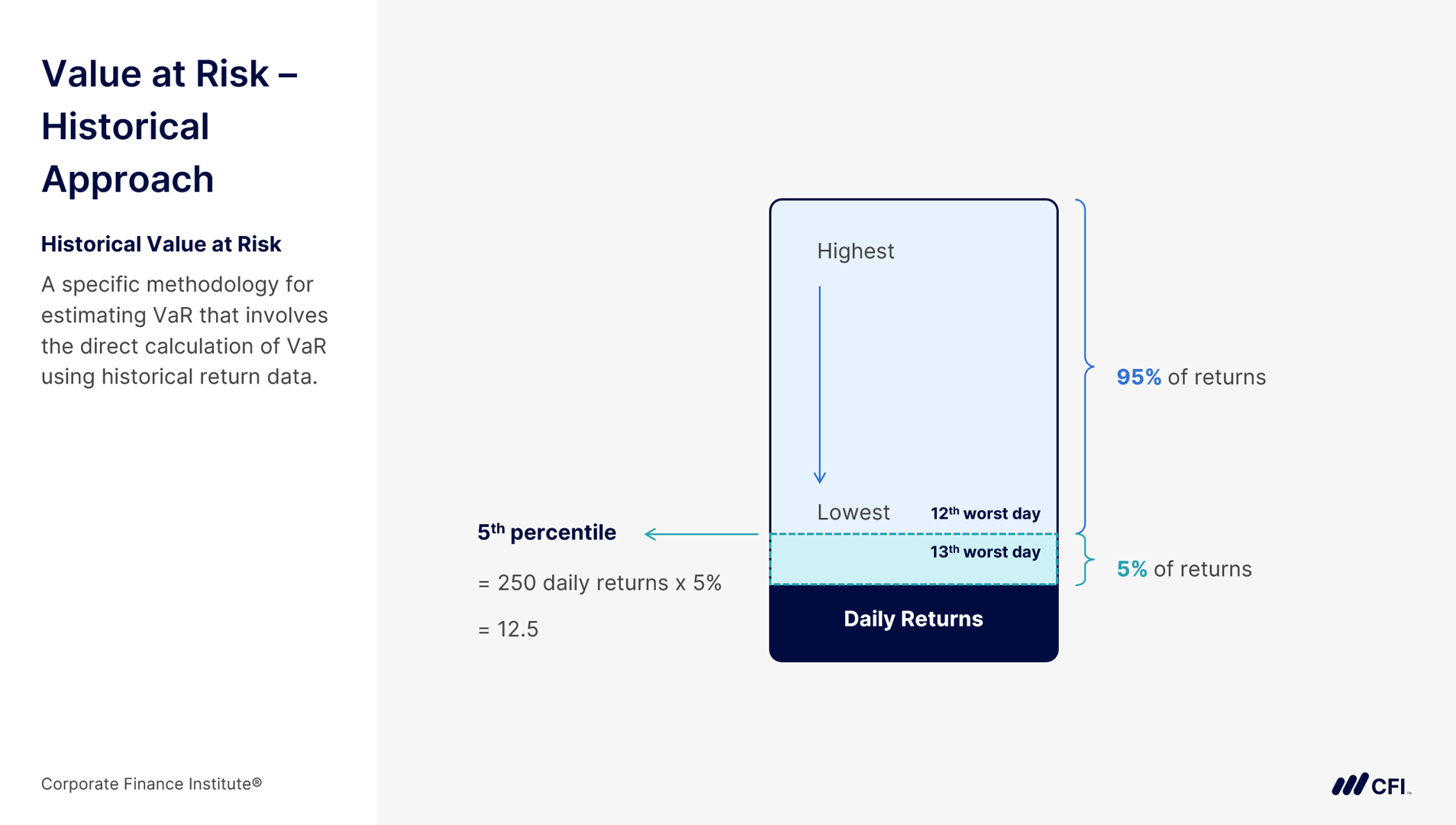

- List reasons why the historical approach is the Value at Risk (VaR), methodology most widely used by financial institutions

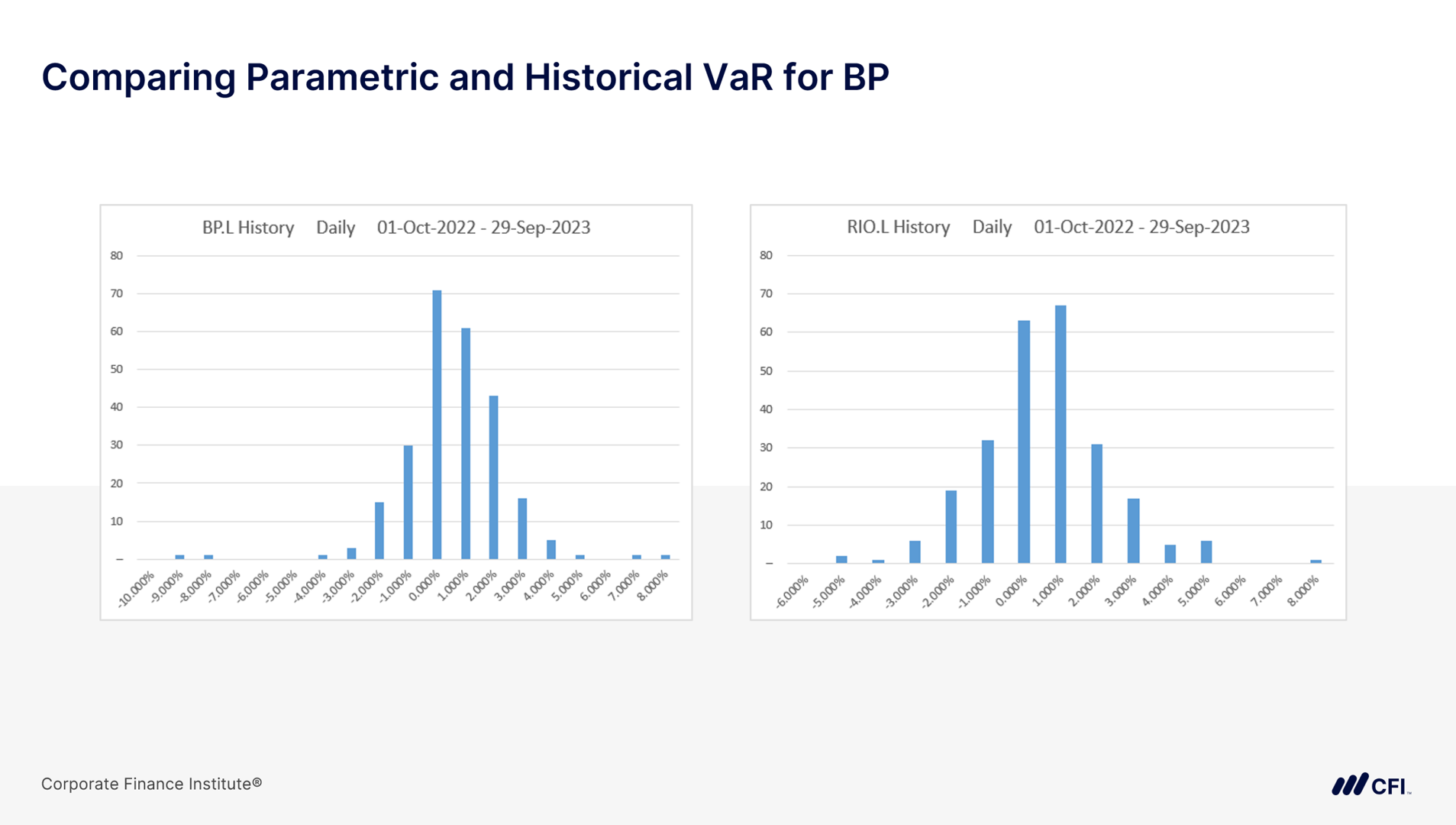

- Calculate Historical VaR for equities in Excel using historical price data

- Calculate the duration for a bond and use this to estimate changes in the bond’s price

- Differentiate between Rate VaR and Price VaR with respect to bonds

- Calculate VaR for bonds in Excel using historical market data

Who Should Take This Course?

This course is ideal for financial professionals, risk managers, and analysts who want to deepen their understanding of market risk assessment using the Historical VaR method. It is also suited for those seeking practical experience in applying VaR calculations to both equity and fixed income securities in real-world scenarios.

Historical VaR for Market Risk

Level 4

Approx 4h to complete

100% online and self-paced

Get Started