Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The accounting for convertible debt interest expense differs between US GAAP and IFRS

A convertible bond is a type of debt security that gives an investor the right to exchange the bond for a predetermined number of shares in the issuing company, at certain times over the bond’s lifetime. It is a hybrid security that possesses features of both debt and equity.

Because investors receive potential upside by participating in the equity of the company, investors usually only require a small coupon payment (or sometimes no coupon payment).

However, accounting for convertible bonds can be quite complicated, with significant differences between US GAAP and IFRS.

Until recently, accounting for convertible bonds was roughly the same under both US GAAP and IFRS. However, US GAAP changed the calculation requirements for simplification purposes.

For the purpose of this article, we will assume that the convertible bond may only be converted to equity and not into another liability (which may occur if the bond is cash settled or has some other complicating features). Additionally, we will assume the bond is issued at the end of the year and makes annual coupon payments (instead of semi-annual).

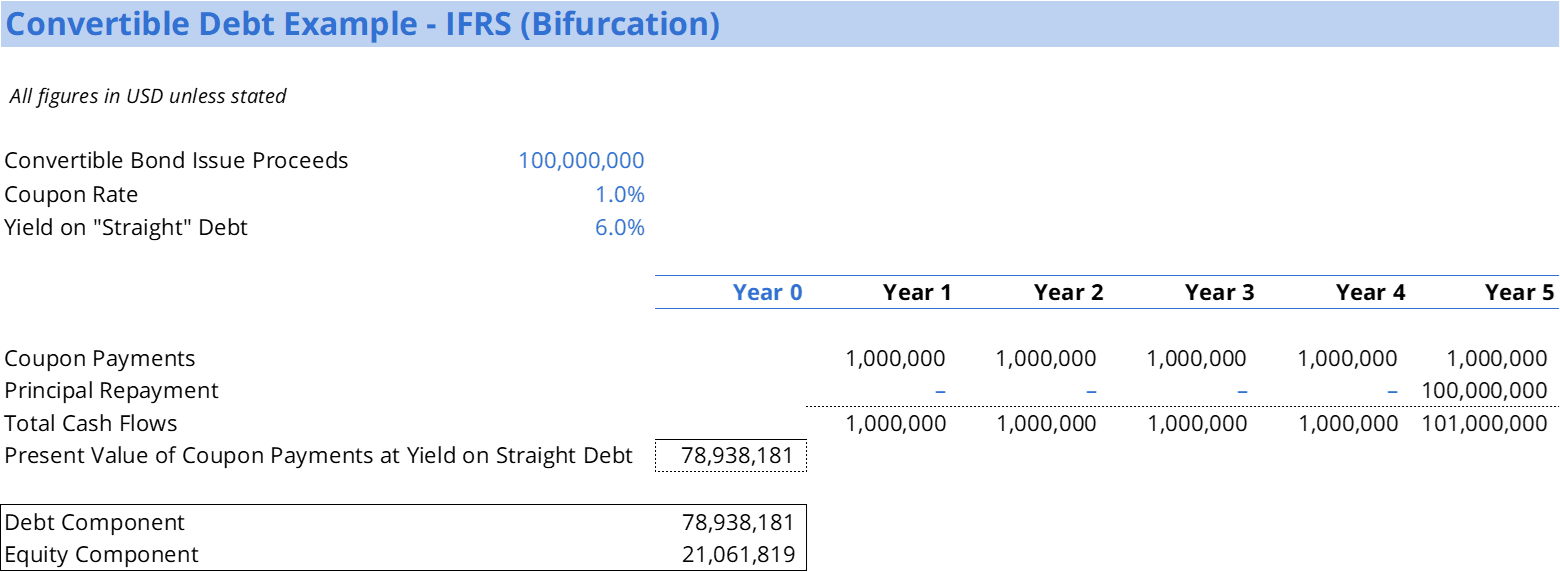

Because convertible debt is a hybrid security, IFRS requires the convertible bond to be bifurcated, creating a debt component and an equity component. The debt component is calculated by discounting the coupon and principal payments at the company’s cost of “straight” debt (regular debt with no conversion option).

Assuming a company issues a 5-year, $100,000,000 convertible bond with a 1% coupon rate, and a 6% “straight” cost of debt, then the present value of the coupon and principal payments is $78,938,181: this is the debt liability (again, assuming end-of-year, annual coupons). To calculate the equity portion of $21,061,819, take the $100,000,000 in proceeds and subtract $78,938,181.

The journal entries at issuance are shown below:

Please download the template to review the calculations.

Enter your name and email in the form below and download the free template now!

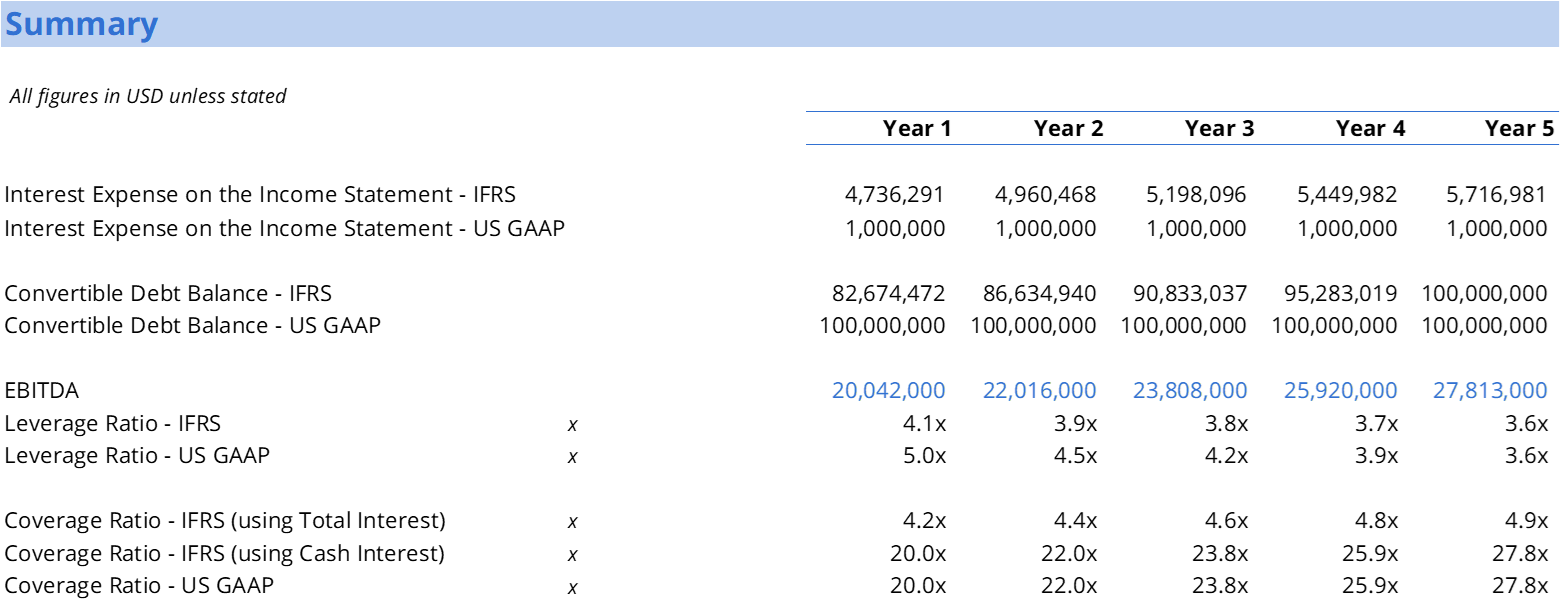

The interest expense is calculated using the 6% cost of straight debt times the beginning balance of the debt liability. In Year 1, the hypothetical interest expense is $4,736,291 (6% * $78,938,181). Since there is a coupon payment of $1,000,000 (1% * $100,000,000), the difference between the interest expense and the coupon payment is “accreted” to the debt liability. In other words, the difference is added to the debt balance. By the end of Year 5 (maturity), the debt liability will be the full $100,000,000.

The interest expense on the income statement in Year 1 is $4,736,291, but only $1,000,000 is actually paid in cash. The accretion amount of $3,736,291 is non-cash interest expense and is added back to net income on the cash flow statement.

Once the bond matures, the investors will be paid back the $100,000,000 if the conversion option is out-of-the-money.

On the other hand, if the option is in-the-money, then investors will exchange the debt for equity and the journal entries would be as follows (for simplicity we will assume the convertible debt investors will only receive company stock if they decide to convert; however, this may not always be the case in reality).

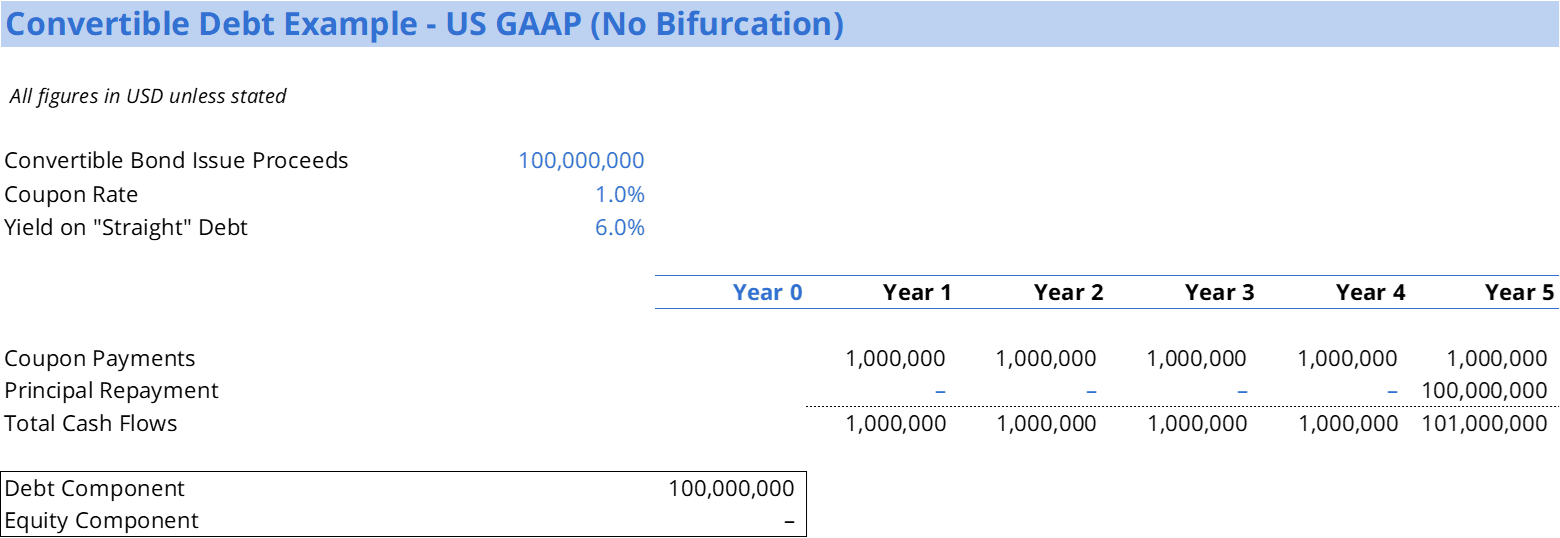

Formerly, US GAAP used to bifurcate convertible debt into debt and equity components but had several, more complicated approaches depending on the structure of the convertible. However, US GAAP no longer uses the bifurcation model and instead assumes the convertible debt is straight debt.

The journal entries at issuance are as follows:

Under US GAAP, the coupon is recognized as interest expense; there is no accretion like under the IFRS model (again, we are simplifying this for illustrative purposes as there may be other debt issuance costs that are included in interest expense).

Like IFRS, if the conversion is not favorable to investors, they will simply receive the principal proceeds at maturity.

However, if the conversion is in-the-money, then the investors will convert to common equity.

Before the change in US GAAP, convertible instruments could use the treasury stock method when calculating diluted earnings per share (EPS). However, the new guidance requires companies to calculate diluted EPS using the if-converted method (this method assumes the entire liability is settled by the company issuing new shares).

Consequently, diluted EPS will now usually be lower under the new accounting guidance (the if-converted method results in a higher share count than the treasury stock method so earnings per share will be lower).

In summary, US GAAP will show a higher debt balance but lower interest expense vs an IFRS-reporting company (at least until the point of maturity). For analysis purposes, leverage ratios (Debt/EBITDA) will be higher under US GAAP, as will coverage ratios (EBITDA/Interest).