Get Specialized with our Financial Planning & Analysis (FP&A) Program

Support business leaders in their decision-making with best-in-class financial models to evaluate and forecast the financial performance of a company.

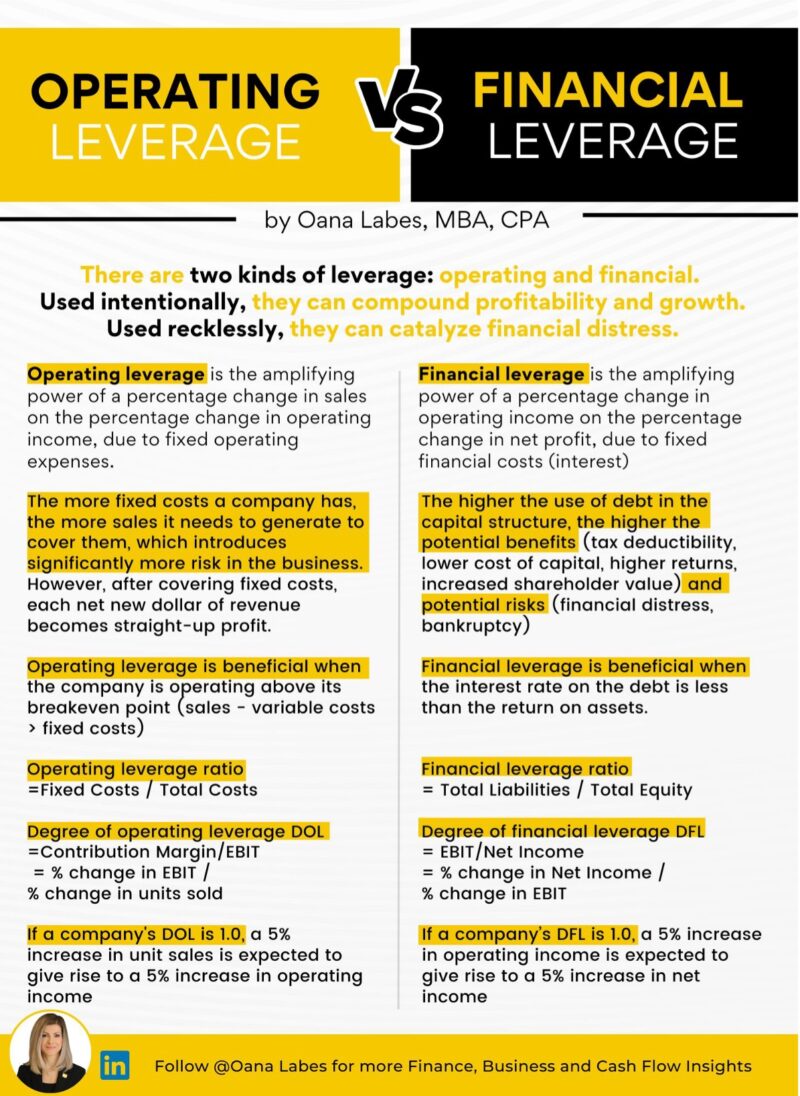

Key to business profitability or catalyst to financial distress

Companies have two main controls to improve business profitability and avoid financial distress. Used intentionally, they can compound profitability and growth. Used recklessly, they can catalyze financial distress. That’s because operating leverage and financial leverage have the power to amplify a company’s earnings in both directions.

Operating leverage is the amplifying power of a percentage change in sales on the percentage change in operating income due to fixed operating expenses, such as rent, payroll or depreciation.

The more fixed costs a company has, the more sales it needs to generate to cover them, and that introduces significant risk into the business. In the event the company can’t generate sufficient revenue and gross margin to offset its fixed costs, it will incur an operating loss.

The effects of an operating loss are extensive, and depending on the presence of other contributing factors, they could include:

On the other side of the challenge to cover a higher fixed cost base, operating leverage affords companies major upside opportunities. After covering fixed costs, each new dollar of revenue net of variable product costs will become straight-up profit, because fixed costs have already been covered for the entire period.

That’s the beauty of operating leverage.

High Fixed Costs > Low Variable Costs > High Gross Margins > High Operating Leverage

Operating leverage is beneficial when the company is operating above its breakeven point (revenue – variable costs > fixed costs).

Operating Leverage Ratio = Fixed Costs / Total Costs

The degree of operating leverage (DOL) calculates the percent change in EBIT expected based on a certain percent change in units sold.

DOL = Contribution Margin / EBIT

A DOL of 1 means that a 1% change in the number of units sold will result in a 1% change in EBIT (operating income).

Financial leverage is the amplifying power of a percentage change in operating income on the percentage change in net profit due to fixed financial costs.

Financial leverage picks up where operating leverage leaves off and is produced through the use of borrowed capital, which generates fixed financial costs (such as interest expense).

The higher the use of debt in the capital structure, the higher the potential shareholder value creation but also shareholder value destruction. The potential benefits of leverage include:

Potential risks of using leverage include:

Financial Leverage Ratio = Total Liabilities / Total Equity

For example, if you’ve got balance sheet liabilities of $4,500,000 and total equity of $8,500,000, your leverage is 0.53 or 0.53:1. If the reverse was true, your leverage would be 1.89 or 1.89:1.

Financial leverage is beneficial when the interest rate on the debt is less than the return on assets. Otherwise, you’re not going to be able to generate a large enough return on the use of the business assets to offset interest borrowing costs.

The degree of financial leverage (DFL) measures the percent change in net income based on a certain percent change in EBIT.

DFL = EBIT / Net Income

If a company’s DFL is 1.0, a 5% increase in operating income is expected to give rise to a 5% increase in net income.

Together, the degree of operating leverage and the degree of financial leverage make up the degree of total leverage.

DTL = DOL + DFL

During periods of economic slowdown, a high degree of leverage can greatly increase business risk and its probability of financial distress. Steps you can take to protect your business under such circumstances include: