Dilution

The reduction of ownership percentage of existing shareholders in a company when new shares are issued by the company

What is Dilution?

Dilution refers to the reduction in the percentage of existing shareholders’ ownership in a company when it issues new shares of stock. It is also referred to as equity or stock dilution. Dilution occurs when optionable securities, such as employee stock options, are exercised.

Summary

- Dilution refers to the reduction of ownership percentage of existing shareholders in a company when new shares are issued by the company.

- Some companies may issue new shares for receiving additional capital for growth opportunities or paying off debts.

- Dilution reduces the book value of the shares and the earnings per share, which may lower the stock prices.

How Dilution Works

When a company goes public, usually through an initial public offering (IPO), a certain number of shares are sanctioned to be offered initially. The outstanding shares are termed as “float.” If the company issues additional shares – known as a secondary stock offering – the company is said to have diluted the stock.

Since the share of a company’s stock represents the ownership stake in the company, the shareholders who purchased the IPO will now have a smaller stake in the ownership of the company.

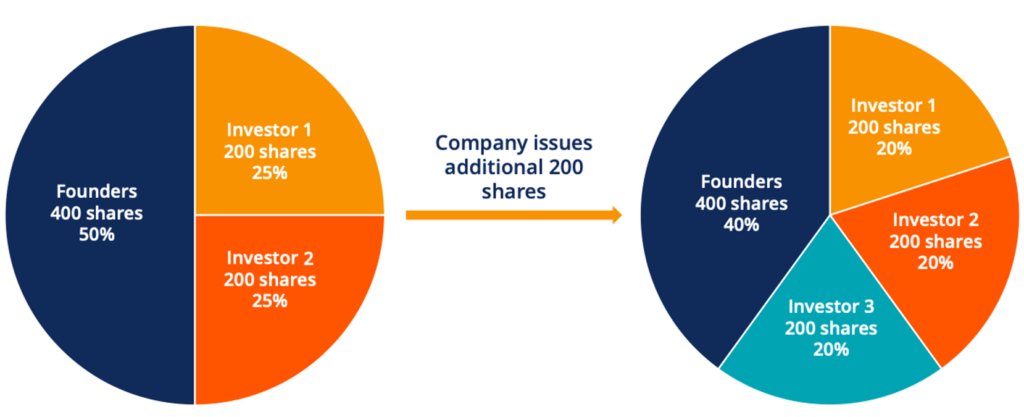

For example, assume that a company issues 100 shares to 100 independent shareholders, with each shareholder having 1% ownership in the company. If the company issues 100 more shares to 100 other shareholders, the ownership of each shareholder reduces to 0.5%. That is because there are now 200 shares outstanding, so 1 share equals 0.5% ownership of the company.

It also reduces the voting power of the shareholders. With the increase in the number of shares, each existing shareholder owns a smaller percentage of the company, resulting in a decrease in the value of each share.

Normally, existing shareholders do not favor the dilution of shares or equity; hence, sometimes, companies take initiatives, such as share repurchase programs, to limit dilution. Stock dilution should not be confused with stock splits, which neither decrease nor increase dilution. When a company enacts stock splits, current shareholders receive extra shares without any effect on their ownership percentage in the company.

Cause of Share Dilution

Although dilution decreases the value of shares, companies still issue additional shares. Some of the causes of dilution are listed below:

- Some companies may issue extra shares to seek additional capital for growth opportunities or to settle outstanding debts. The value of the company’s stock and its profitability can be improved through the capital received from issuing new shares in the stock market.

- A company purchasing another company may issue additional shares to the shareholders of the acquired company.

- A company may offer stock options to its employees and other optionable securities. When the stock options are exercised, they are converted into shares of the company. Thus, the number of outstanding shares of the company increases.

- Smaller companies may sometimes issue shares to independent service providers.

- Some companies may issue warrants or other convertible securities, such as bonds. Warrants are usually issued to lenders. When the securities are converted, new shares are added to the pool of outstanding shares of the companies.

- Shareholders with a major stake in the company can use share dilution to remove other shareholders with less stake in the company or to get the latter’s consent to the plans that normally they would not agree to.

Effect of Dilution

Dilution affects the value of a portfolio depending on the number of additional shares issued and the number of shares held. Dilution not only affects the share price but also the earnings per share (EPS) of the company.

For example, a company’s EPS may be 50 cents per share before the issuance of additional shares, and it may reduce to 18 cents after dilution. However, the EPS may not be affected if the dilution causes a significant increase in earnings. The funds from dilution may help boost revenue, which can offset the increase in the number of shares, and the EPS may not change.

Public companies may also calculate diluted EPS to determine the potential effect of dilution on stock prices in case stock options are exercised. Dilution results in a decline in the book value of the shares and the earnings per share of the company.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: