Get Certified for

Capital Markets (CMSA®)

From equities, fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A market-neutral strategy that seeks to take advantage of market inefficiencies between a commodity's spot price and its future price

Reverse cash and carry arbitrage is the inverse of the cash and carry arbitrage commodity trading strategy. Like cash and carry arbitrage, it is a market-neutral strategy that seeks to take advantage of market inefficiencies between a commodity’s spot price and its future price.

In the reverse cash and carry arbitrage strategy, the trader takes a short position in the spot price of a commodity and a long position on its future price. It is different from being short in equities. In commodities trading, the trader must consider the storage and carry cost when calculating the value in a commodity’s future price and deciding if the strategy is worthwhile.

A normal market where commodity futures prices are higher than spot commodity prices is called a contango market. In a contango market, there is an upward sloping futures curve. In a market where there is a downward sloping futures curve, futures pricing is called backwardation. It is the type of market where reverse cash and carry arbitrage is heavily utilized.

Backwardation is not as common as the contango market, as futures prices generally consider storage and carry costs. The abnormality of backwardation sees traders attempting to take advantage of this pricing irregularity and taking a profit.

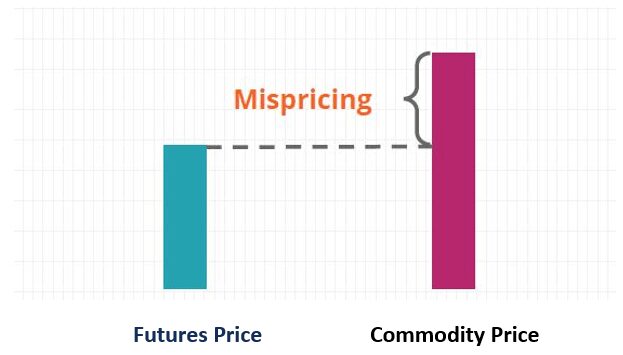

The diagram below represents the mismatch in pricing we see in reverse cash and carry arbitrage. For more information about the image, check out CFI’s Introduction to Commodities course.

Traders utilize cash and carry arbitrage across a wide variety of commodities. We will use wheat for our below example. Wheat is currently priced at $204 per contract (5000 bushels). The one-year future price for wheat is currently $200. Yearly carrying costs are $3 per annum on the contract.

A trader utilizing reverse cash and carry arbitrage would short wheat that currently trades at $204 (spot) and purchase the one-year future contract at $200 dollars. They would then profit $1 dollar per contract. The calculation is as follows: $204 – $200 – $3 = $1.

Utilizing the above trading style to take advantage of mismatches in the market is not without inherent risks. For example, the carrying costs could fluctuate within the one-year timeframe. As such, traders practicing reverse cash and carry must also be aware of potential fluctuations in the external costs that could impact the profitability of a trade significantly.

Commodities trading that uses methods like reverse cash and carry arbitrage requires a strong understanding of the internal and external forces that can influence a market.

To understand if mispricing is occurring, one must understand all the additional costs that can influence the reverse carry portion of an arbitrage deal. In traditional commodities trading, some of the typical costs that must be considered that can influence the profitability of a deal are:

CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: