Get Certified for

Capital Markets (CMSA®)

From equities, fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Derivative contracts that gives the holder the right, but not the obligation, to buy or sell an asset by the expiration date for the strike price

An option is a derivative, a contract that gives the buyer the right, but not the obligation, to buy or sell the underlying asset by a certain date (expiration date) at a specified price (strike price). There are two types of options: calls and puts. American-style options can be exercised at any time prior to their expiration. European-style options can only be exercised on the expiration date.

To enter into an option contract, the buyer must pay an option premium. The two most common types of options are calls and puts:

Calls give the buyer the right, but not the obligation, to buy the underlying asset at the strike price specified in the option contract. Investors buy calls when they believe the price of the underlying asset will increase and sell calls if they believe it will decrease.

Puts give the buyer the right, but not the obligation, to sell the underlying asset at the strike price specified in the contract. The writer (seller) of the put option is obligated to buy the asset if the put buyer exercises their option. Investors buy puts when they believe the price of the underlying asset will decrease and sell puts if they believe it will increase.

The buyer of a call option pays the option premium in full at the time of entering the contract. Afterward, the buyer enjoys a potential profit should the market move in his favor. There is no possibility of the option generating any further loss beyond the purchase price. This is one of the most attractive features of buying options. For a limited investment, the buyer secures unlimited profit potential with a known and strictly limited potential loss.

If the spot price of the underlying asset does not rise above the option strike price prior to the option’s expiration, then the investor loses the amount they paid for the option. However, if the price of the underlying asset does exceed the strike price, then the call buyer makes a profit. The amount of profit is the difference between the market price and the option’s strike price, multiplied by the incremental value of the underlying asset, minus the price paid for the option.

For example, a stock option is for 100 shares of the underlying stock. Assume a trader buys one call option contract on ABC stock with a strike price of $25. He pays $150 for the option. On the option’s expiration date, ABC stock shares are selling for $35. The buyer/holder of the option exercises his right to purchase 100 shares of ABC at $25 a share (the option’s strike price). He immediately sells the shares at the current market price of $35 per share.

He paid $2,500 for the 100 shares ($25 x 100) and sells the shares for $3,500 ($35 x 100). His profit from the option is $1,000 ($3,500 – $2,500), minus the $150 premium paid for the option. Thus, his net profit, excluding transaction costs, is $850 ($1,000 – $150). That’s a very nice return on investment (ROI) for just a $150 investment.

The call option seller’s downside is potentially unlimited. As the spot price of the underlying asset exceeds the strike price, the writer of the option incurs a loss accordingly (equal to the option buyer‘s profit). However, if the market price of the underlying asset does not go higher than the option strike price, then the option expires worthless. The option seller profits in the amount of the premium they received for the option.

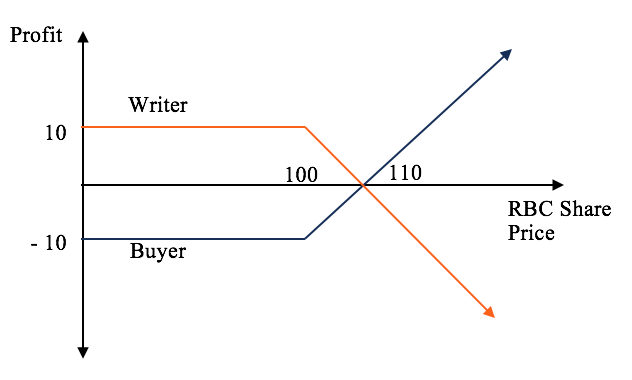

An example is portrayed below, indicating the potential payoff for a call option on RBC stock, with an option premium of $10 and a strike price of $100. In the example, the buyer incurs a $10 loss if the share price of RBC does not increase past $100. Conversely, the writer of the call is in-the-money as long as the share price remains below $110.

A put option gives the buyer the right to sell the underlying asset at the option strike price. The profit the buyer makes on the option depends on how far below the spot price falls below the strike price. If the spot price is below the strike price, then the put buyer is “in-the-money.” If the spot price remains higher than the strike price, the option will expire unexercised. The option buyer’s loss is, again, limited to the premium paid for the option.

The writer of the put is “out-of-the-money” if the spot price of the underlying asset is below the strike price of the contract. Their loss is equal to the put option buyer’s profit. If the spot price remains above the strike price of the contract, the option expires unexercised, and the writer pockets the option premium.

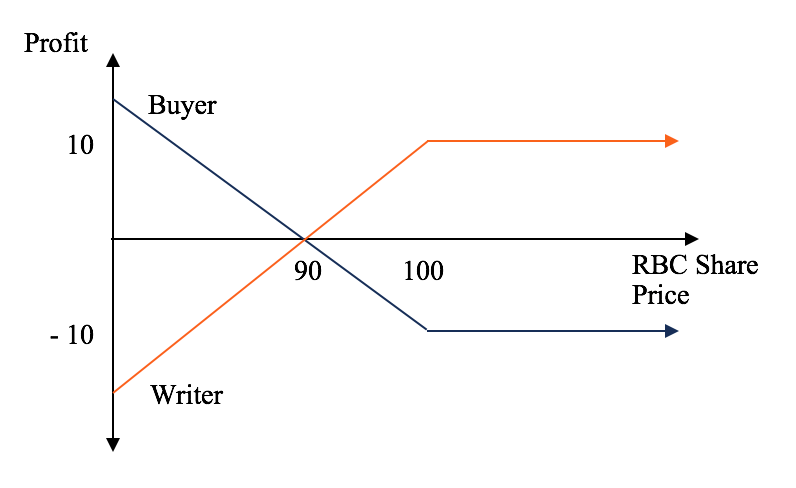

Figure 2 below shows the payoff for a hypothetical 3-month RBC put option, with an option premium of $10 and a strike price of $100. The buyer’s potential loss (blue line) is limited to the cost of the put option contract ($10). The put option writer, or seller, is in-the-money as long as the price of the stock remains above $90.

Options: calls and puts are primarily used by investors to hedge against risks in existing investments. It is frequently the case, for example, that an investor who owns stock buys or sells options on the stock to hedge his direct investment in the underlying asset. His option investments are designed to at least partially compensate for any losses that may be incurred in the underlying asset. However, options may also be used as standalone speculative investments.

If an investor believes that certain stocks in their portfolio may drop in price but they do not wish to abandon their position for the long term, they can buy put options on the stock. If the stock does decline in price, then profits in the put options will offset losses in the actual stock.

Investors commonly implement such a strategy during periods of uncertainty, such as earnings season. They may buy puts on particular stocks in their portfolio or buy index puts to protect a well-diversified portfolio. Mutual fund managers often use puts to limit the fund’s downside risk exposure.

If an investor believes the price of a security is likely to rise, they can buy calls or sell puts to benefit from such a price rise. In buying call options, the investor’s total risk is limited to the premium paid for the option. Their potential profit is, theoretically, unlimited. It is determined by how far the market price exceeds the option strike price and how many options the investor holds.

For the seller of a put option, things are reversed. Their potential profit is limited to the premium received for writing the put. Their potential loss is unlimited – equal to the amount by which the market price is below the option strike price, times the number of options sold.

Investors can benefit from downward price movements by either selling calls or buying puts. The upside to the writer of a call is limited to the option premium. The buyer of a put faces a potentially unlimited upside but with a limited downside, equal to the option’s price. If the market price of the underlying security falls, the put buyer profits to the extent the market price declines below the option strike price. If the investor’s hunch is wrong and prices don’t fall, the investor only loses the option premium.

From capital markets to trading and technical analysis strategies, CFI’s 115-page Trading & Investing eBook covers all the major topics a world-class analyst needs to know. Complete the form below to download our free guide!

To keep learning and advance your career, the following resources will be helpful: