Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The fixed monthly payments that borrowers make to lenders to pay down their loans

An equated monthly installment (EMI) is a type of payment made by borrowers to lenders on a monthly basis in a fixed amount. EMIs include both the interest and principal amounts. After a certain number of EMIs are made, the loan will be fully paid off.

Borrowers usually make equated monthly installments (EMIs) for many types of loans, such as student loans, auto loans, and home mortgages. EMIs are made on the same day every month at a fixed amount. The borrower will be able to completely pay off the loan at the end of the loan term if EMIs are made as scheduled.

Compared to variable payment plans, which allow borrowers to make payments at their discretion based on their periodic incomes, EMIs have a clear repayment schedule and term to maturity.

EMIs consist of contributions of both interest and principal, but the composition of each EMI changes over time, and, at the end of the loan term, the loan will be paid down completely.

The calculation of EMI requires three inputs: the total principal amount, interest rate, and term of the loan. There are two methods to calculate EMI: the flat-rate method and the reduce-balancing method.

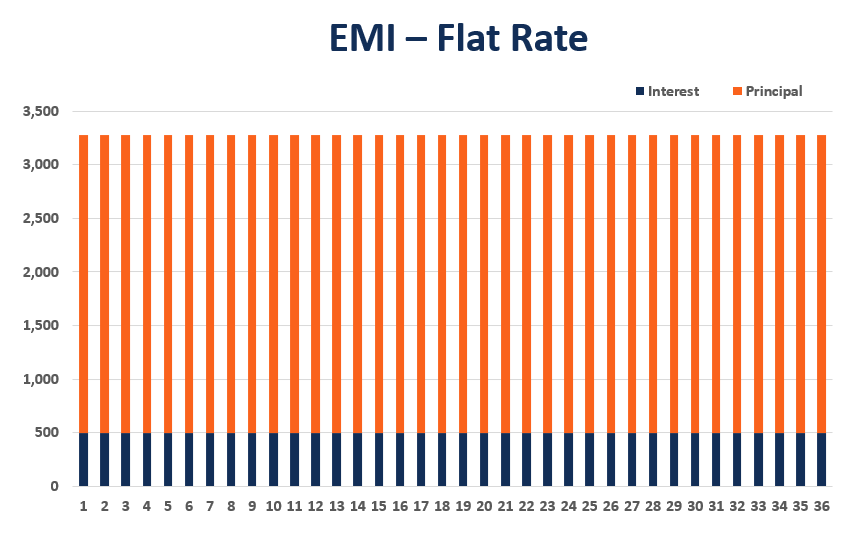

In the flat-rate method, each interest charge is calculated based on the original loan amount, even though the loan balance outstanding is gradually being paid down. The EMI amount is calculated by adding the total principal of the loan and the total interest on the principal together, then dividing the sum by the number of EMI payments, which is the number of months during the loan term.

For example, a borrower takes a $100,000 loan with a 6% annual interest rate for three years. The total amount of interest during the loan term will be $18,000 (6% * $100,000 * 3), which will be $500 monthly. The EMI amount will be $3,278 [($100,000 + $18,000) / 36]. Thus, the contribution to the principal of each EMI will be $2,778 ($3,278 – $500), which makes up 85% of each EMI, as the interest payment makes up the rest of 15%.

The flat-rate method is particularly used on personal loans and vehicle loans. It is less favorable to borrowers since the interest payments must be made for the entire principal amount, which leads to a higher effective interest rate compared to the reducing-balance method.

In contrast to the flat-rate method, the reducing-balance method calculates the interest payment based on the principal outstanding. It means the interest and principal repayment portions of each EMI change overtime. At the early stage of the loan term, interest payment makes up a greater portion of the EMI, as a certain percentage of the loan outstanding.

As the loan is gradually repaid over time, the interest amount reduces, and a greater proportion of the contributions are made towards principal repayments. The reducing-balance method is commonly used on housing mortgages, credit cards, and overdraft facilities.

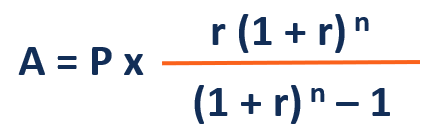

The reducing-balance EMI can be calculated through the formula below:

Where:

In the reducing-balance method, the EMI payment of the example above will change to $3,040, calculated as below:

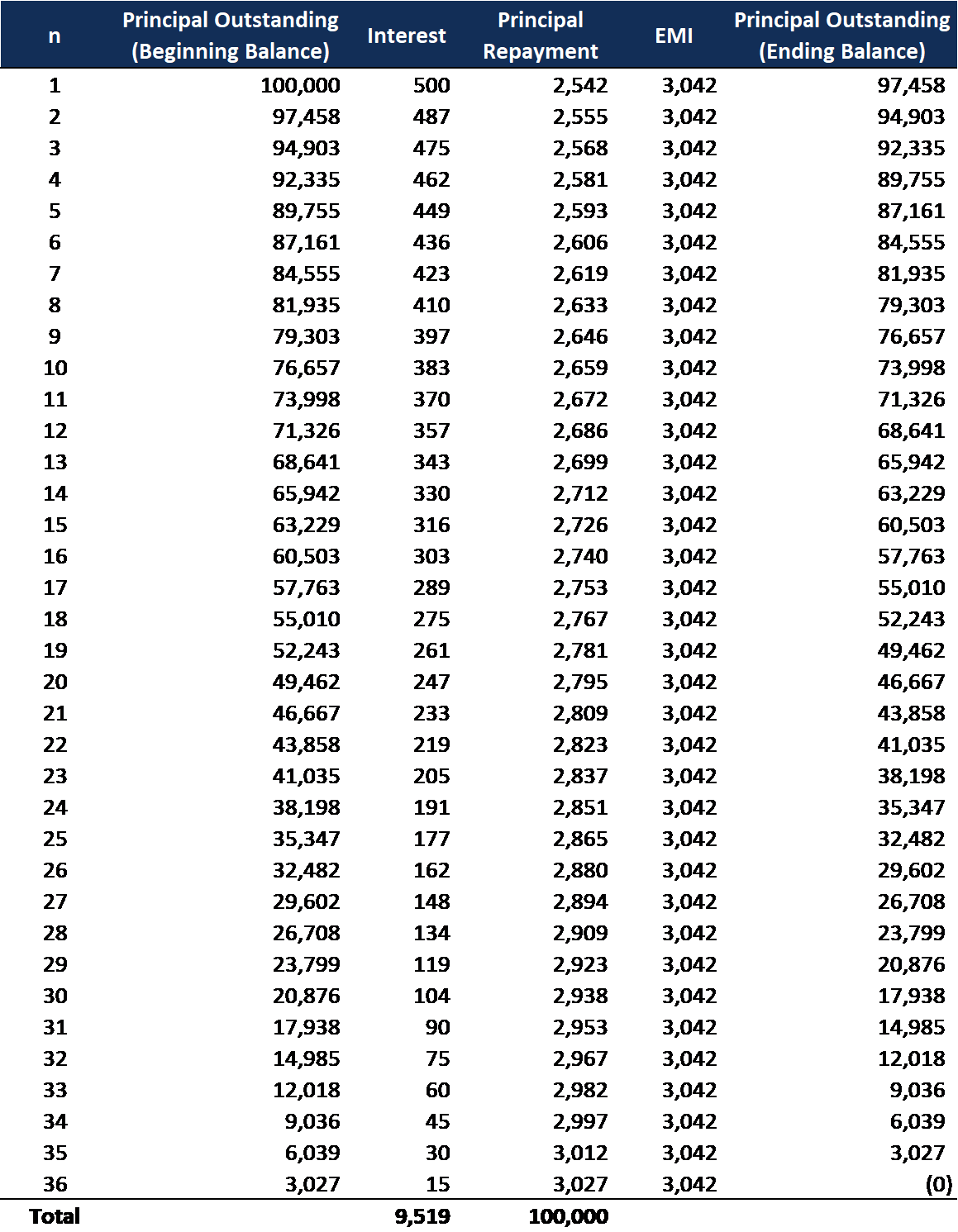

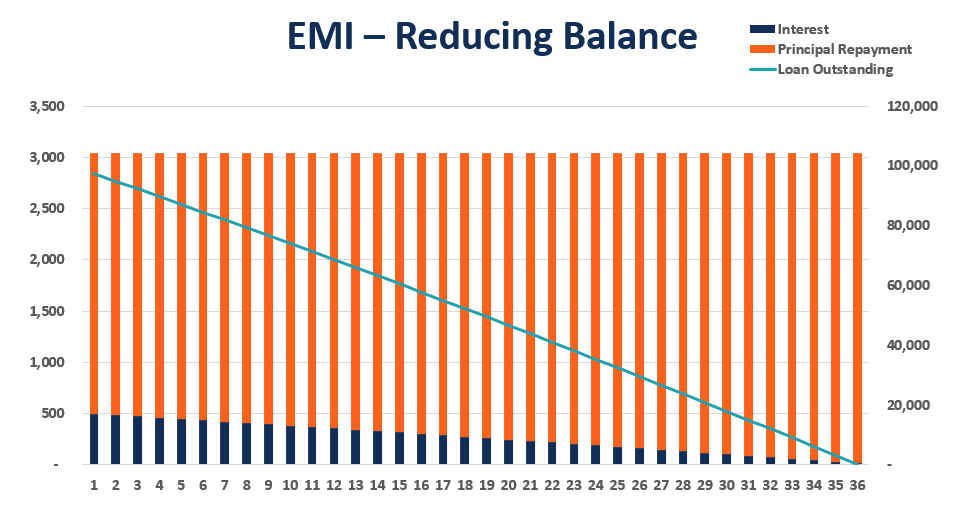

The contribution to interest for the first EMI payment is $500 ($100,000 * 0.5%), and the principal repayment is thus $2,542 ($3,042 – $500). For the second month, the interest repayment reduces to $487 [($100,000 – $2,542) * 0.5%], and the principal repayment thus increases to $2,555. The rest of the payments can be calculated with the same method. The repayment schedule is shown in the table below:

As the diagram below shows, the interest portion declines gradually with the loan outstanding, which will be completely paid out and reduced to zero at the 36th month. Here, the total amount of interest payment is $9,519, which is much lower compared to the $18,000 under the flat-rate method. It makes the reducing-balance method more favorable to borrowers.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: