Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

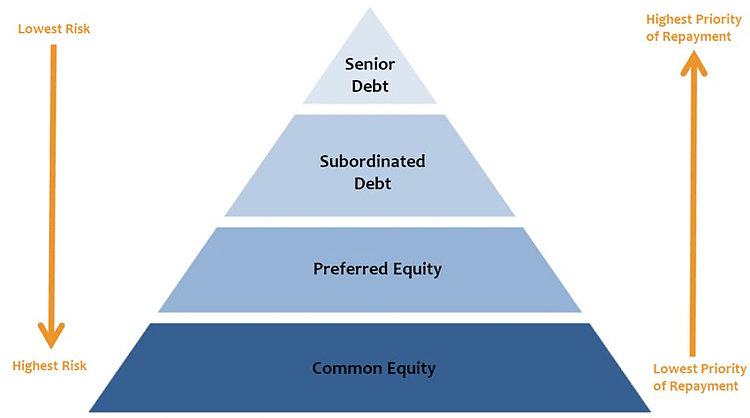

Debt with claim priority

Senior Debt, or a Senior Note, is money owed by a company that has first claims on the company’s cash flows. It is more secure than any other debt, such as subordinated debt (also known as junior debt), because senior debt is usually collateralized by assets. It means the lender is granted a first lien claim on the company’s property, plant, or equipment in the event that the company fails to fulfill its repayment obligations.

The most common types of senior debt are Senior Term Debt and Revolving Credit Facility. They are provided by the commercial or corporate banking departments of a bank.

As shown in the diagram above, financing the company through senior debt provides the lowest risk and highest priority of repayment for the lender, as compared to other types of debt. Debtholders, typically bondholders and banks, are entitled to repayment before shareholders, should the company go through bankruptcy and liquidation.

As it is borrowed money, each layer of debt has a corresponding interest rate payment schedule, where the company will make regular principal and interest payments. Moreover, to try to avoid potential insolvency by the borrower, senior debtholders may prevent the company from issuing junior debts. If so, this is stated in senior debt covenants that are designed to provide extra protection against a loss for the lender.

Debt covenants are agreements between the borrower and lender that can be rather restrictive. For example, the borrowing company may be required to maintain a designated credit profile. This is achieved by targeting a certain level of leverage ratios, such as the debt service coverage and interest service coverage ratios.

The company may also be required to maintain certain business activities or to refrain from any activities or investments that are outside of its core business operations. If the borrower does not abide by the covenant, then the lender has the right to either rescind the loan and demand immediate repayment of accrued interest and principal, or to make changes to the loan agreement, such as increasing the interest rate charged for the loan.

Since senior debt is considered a safer investment, lenders receive the least amount of return for it. Unlike senior debt, when banks take on some junior debt of a company, they will charge higher interest rates to compensate for the risk of having a subordinate status.

Senior debt is accessible by various businesses and widely offered by major banks. These banks generally have a low cost of funding and a profitable spread between this cost and the interest rate they charge to their borrowers.

Furthermore, to maintain a healthy financial system, financial regulators implement standards and requirements that encourage banks to take less risk and focus more on offering “senior” financial products.

Unsecured debt is different in that it does not have a pledged asset as collateral. Instead, the debtholders have a general claim against the company’s assets. If the company goes bankrupt, unsecured senior debtholders are first in line to get paid off from the assets of the company, excluding any pledged assets for secured senior debtholders. Any remaining assets, after senior debtholders have been paid, will then go to the subordinated debtholders.

CFI offers the Commercial Banking & Credit Analyst (CBCA)® certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: