Get Certified for

Capital Markets (CMSA®)

From equities, fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Core capital that a bank holds in its capital structure

Common Equity Tier 1 (CET1) is a component of Tier 1 Capital, and it encompasses ordinary shares and retained earnings. The implementation of CET1 started in 2014 as part of Basel III regulations relating to cushioning a local economy from a financial crisis.

The Basel III accord introduced a regulation that requires commercial banks to maintain a minimum capital ratio of 8%, 6% of which must be Common Equity Tier 1. The Tier 1 capital ratio should comprise at least 4.5% of CET1. The Basel III accord was introduced in 2009 as a response to the 2008 Global Financial Crisis and as part of continuous efforts to improve the banking regulatory framework.

The 2008 Global Financial Crisis occurred during the period when the Basel II accord was being implemented. Basel II established risk and capital management requirements that ensured that banks maintained adequate capital equivalent to the risk they were exposed to through their core activities, i.e., lending, investments, and trading.

However, the financial crisis happened before Basel II could become fully effective, prompting calls for more stringent regulations to cushion against the effects of the crisis. The regulations later became part of the Basel III accord, which compared a bank’s assets to its capital to determine its adequacy to survive a period of financial distress.

One of the regulations introduced under the Basel III accord was limiting the type of capital that banks could hold in their capital structure. Banks use the different forms of capital to absorb losses that occur during the regular operations of the business.

The main forms of capital included in the capital structure of a bank include Common Equity Tier 1 Capital, Tier 1 Capital, and Tier 2 Capital. CET1 represents the bank’s core capital. It includes ordinary shares, retained earnings, stock surpluses from the issue of common shares and common shares held by the subsidiaries of the company.

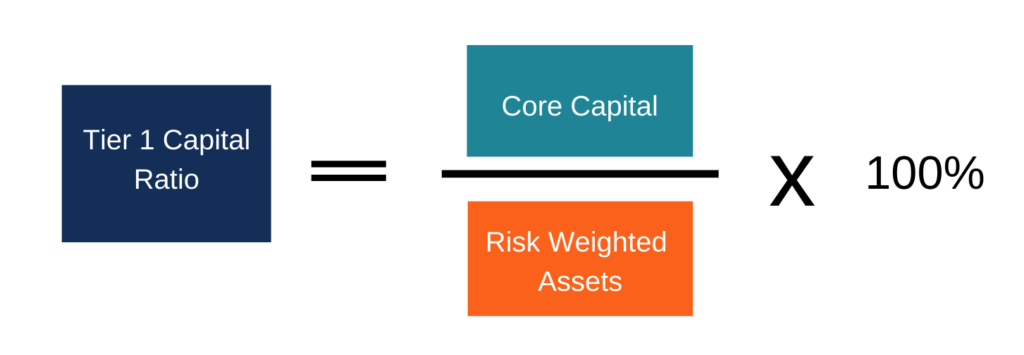

The Tier 1 Capital Ratio is calculated by taking a bank’s core capital relative to its risk-weighted assets. The risk-weighted assets are the assets that the bank holds and that are evaluated for credit risks. The assets are assigned a weight according to their level of credit risk. For example, cash on hand would be weighted 0%, while a mortgage loan would carry weights of 20%, 50%, or 100%.

The Tier 1 Capital Ratio was introduced in 2010 after the financial crisis as a measure of a bank’s ability to withstand financial distress. Most banks held too much debt and low levels of equity, and they lacked adequate capital to absorb losses resulting from the financial crisis. Basel III requires that the equity component of Tier 1 capital should be at least 4.5% of risk-weighted assets.

The formula for calculating Tier 1 capital ratio is as follows:

Example

Assume that ABC Bank holds $2 million in core capital and lends out $10 million to XYZ Limited. The outstanding loan comes with a risk weighting of 80%. The bank’s Tier 1 capital ratio can be calculated as follows:

Therefore, the Tier 1 capital ratio for ABC Bank is 25%. The following are the two main ways of expressing the ratio:

Basel III tightened the capital adequacy requirements that banks are required to observe. The accord categorizes regulatory capital into Tier 1 and Tier 2. Tier 1 comprises Common Equity Tier 1 and an additional Tier 2. Common Equity Tier 1 includes instruments with discretionary dividends, such as common stocks, while additional Tier 1 includes instruments with no maturity and whose dividends can be canceled at any time.

Under Basel III, the minimum Common Equity Tier 1 increased to 4.5%, down from 4% in Basel II. It also increased the minimum Tier 1 capital to 6% from 4% in Basel II. The overall minimum regulatory capital ratio was left unchanged at 8%, out of which 6% is Tier 1 capital. By the end of 2019, banks were required to hold a conservation buffer of 2.5% of the risk-weighted assets, which brings the total Common Equity Tier 1 capital to 7%, i.e., 4.5% + 2.5%.

Thank you for reading CFI’s guide on Common Equity Tier 1 (CET1). To help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: