Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The different sources of synergies

Synergies arise in a merger or acquisition (M&A) when the merged value of the two firms is higher than the pre-merger value of both firms simply added together. For example, if firm A has a value of $500 million, firm B has a value of $75 million, but the combined value of the firm is $625 million, we can say there are $50 million in synergies for this merger ($625 – $500 – $75).

Synergies may arise in M&A transactions for several reasons as there are different types of synergies. The two most common “hard” synergies are cost savings and revenue upside.

However, there are other “soft” synergies that may also arise due to a merger. One example is a common corporate culture that will allow the merged firm to be more easily successful.

Below, we discuss a non-exhaustive list of potential types of synergies that a merged company may be able to realize in a transaction.

Here is a list of cost-saving synergies that can be achieved when two companies merge:

Here is a list of revenue-enhancing synergies that can be achieved when two companies merge:

Financial synergies occur when the merged firm is able to better improve its capital structure compared to when the companies were separate. Capital structure changes potentially result in increased benefits in terms of tax savings and debt capacity. If successful, the merged firm can theoretically reduce its cost of capital, thereby resulting in a higher valuation versus the standalone companies.

Below are examples of financial synergies:

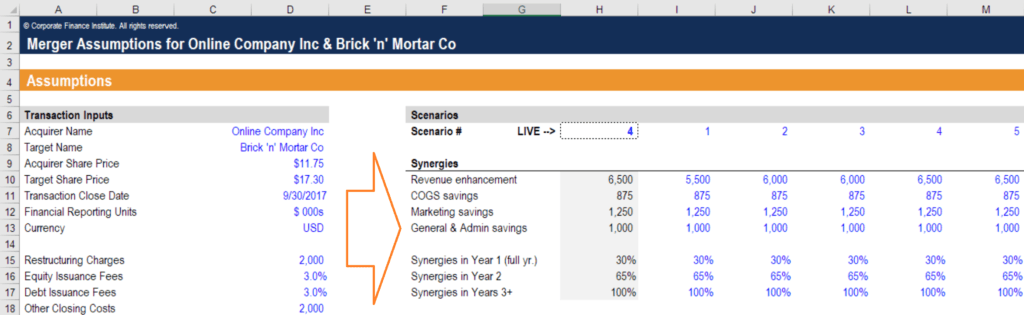

Below is a screenshot of CFI’s Mergers and Acquisitions Modeling Course. As you can see in the lower right corner of the assumptions section, there are various types of synergies that are incorporated into the model, such as revenue enhancements, COGS savings, marketing savings, and G&A savings.

Additionally, it takes time for the merged firm to actually realize synergies. Notice that in our M&A model, it takes three years for the synergies to reach 100% of their potential impact, as shown in cells H15:H17.

One approach to the way merger synergies are forecasted is by comparing like-transactions. In other words, comparable acquisitions are reviewed as a starting point for potential synergies. As an example, let’s assume a comparable transaction assumed synergies would be five percent of the total enterprise value (EV) of the target. If the transaction we are analyzing is truly comparable, we can assume that synergies should be five percent of the EV as well.

However, it may be initially difficult to quantitatively estimate synergies as the operational intricacies of a combination are not yet known until post-merger. Thus, synergies may be first estimated qualitatively.

Another approach is to look internally at the two companies and perform as much analysis as possible. A bottoms-up analysis should be performed to see how the acquiring firm expects the target firm’s assets and operations to line up and what cost savings can be made. This second approach is more detailed and possibly more accurate; however, it’s very challenging for anyone outside of the deal to accurately perform this analysis themselves.

There are two main types of synergies: hard and soft. Hard synergies refer to costs savings, while soft synergies refer to revenue increases and financial synergies.

The reason why they are called hard versus soft is because cost savings are usually much easier to actually realize compared to revenue or financial synergies.

Synergies can also be negative (dis-synergies) if a transaction is poorly executed or integrated. Based on a study by McKinsey, more than 60% of transactions fall short of the synergies they hoped to achieve, and many transactions actually experience negative synergies.

As an example, expected cost savings might actually turn into higher total costs if the two businesses fail to integrate properly.

Alternatively, revenue and marketing synergies may not materialize if the two companies have completely different sales strategies. For example, the Quaker Oats-Snapple deal struggled due to different sales channels (Quaker Oats in large supermarkets, Snapple in small stores or gas stations), in addition to the fact that the products targeted different markets.

Synergies are not effective immediately after the merger takes place. Typically, these synergies are realized one to three years after the transaction. This period is known as the “phase-in” period, where operational efficiencies, cost savings, and incremental new revenues are slowly absorbed into the newly merged firm.

In fact, in the short-term, costs may actually go up as the integration of the two companies will likely incur various non-recurring expenses, as well as short-term inefficiencies due to a lack of history of working together and culture clashes between companies. If a culture clash is too great, synergies may never be realized.

This has been a guide to types of synergies in M&A transactions. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst.

To learn more, see these additional relevant resources below: