Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The value attributable to the owners of a business

In finance and accounting, equity is the value attributable to the owners of a business. The book value of equity is calculated as the difference between assets and liabilities on the company’s balance sheet, while the market value of equity is based on the current share price (if public) or a value that is determined by investors or valuation professionals. The account may also be called shareholders/owners/stockholders equity or net worth.

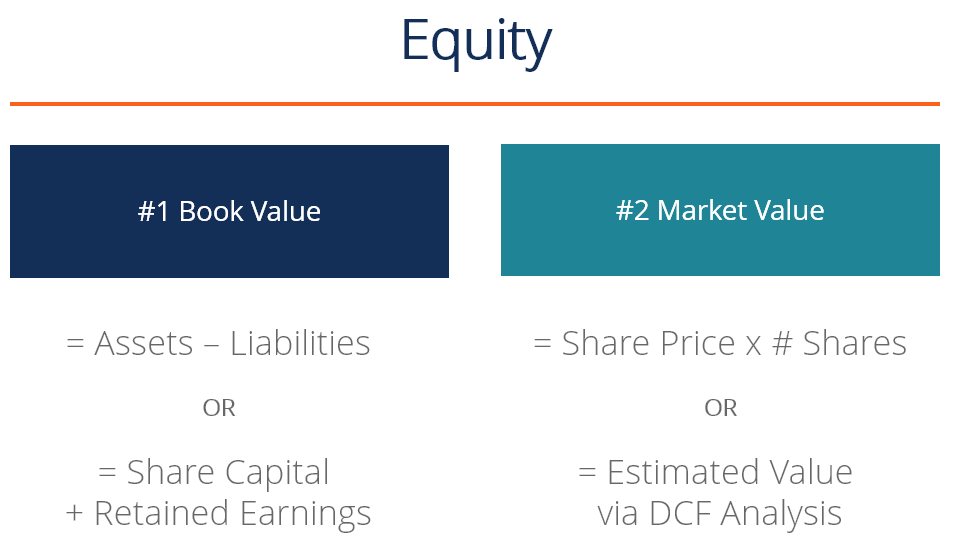

There are generally two types of equity value:

In accounting, equity is always listed at its book value. This is the value that accountants determine by preparing financial statements and the balance sheet equation that states: assets = liabilities + equity. The equation can be rearranged to: equity = assets – liabilities.

The value of a company’s assets is the sum of each current and non-current asset on the balance sheet. The main asset accounts include cash, accounts receivable, inventory, prepaid expenses, fixed assets, property plant and equipment (PP&E), goodwill, intellectual property, and intangible assets.

The value of liabilities is the sum of each current and non-current liability on the balance sheet. Common liability accounts include lines of credit, accounts payable, short-term debt, deferred revenue, long-term debt, capital leases, and any fixed financial commitment.

In reality, the value of equity is calculated in a much more detailed way and is a function of the following accounts:

To fully calculate the value, accountants must track all capital the company has raised and repurchased (its share capital), as well as its retained earnings, which consist of cumulative net income minus cumulative dividends. The sum of share capital and retained earnings is equal to equity.

In finance, equity is typically expressed as a market value, which may be materially higher or lower than the book value. The reason for this difference is that accounting statements are backward-looking (all results are from the past) while financial analysts look forward, to the future, to forecast what they believe financial performance will be.

If a company is publicly traded, the market value of its equity is easy to calculate. It’s simply the latest share price multiplied by the total number of shares outstanding.

If a company is private, then it’s much harder to determine its market value. If the company needs to be formally valued, it will often hire professionals such as investment bankers, accounting firms (valuations group), or boutique valuation firms to perform a thorough analysis.

If a company is private, the market value must be estimated. This is a very subjective process, and two different professionals can arrive at dramatically different values for the same business.

The most common methods used to estimate equity value are:

In the discounted cash flow approach, an analyst will forecast all future free cash flow for a business and discount it back to the present value using a discount rate (such as the weighted average cost of capital). DCF valuation is a very detailed form of valuation and requires access to significant amounts of company information. It is also the most heavily relied on approach, as it incorporates all aspects of a business and is, therefore, considered the most accurate and complete measure.

To learn more, read CFI’s guide to business valuation resources.

The concept of equity applies to individual people as much as it does to businesses. We all have our own personal net worth, and a variety of assets and liabilities we can use to calculate our net worth.

Common examples of personal assets include:

Common examples of personal liabilities include:

The difference between all your assets and all your liabilities is your personal net worth.

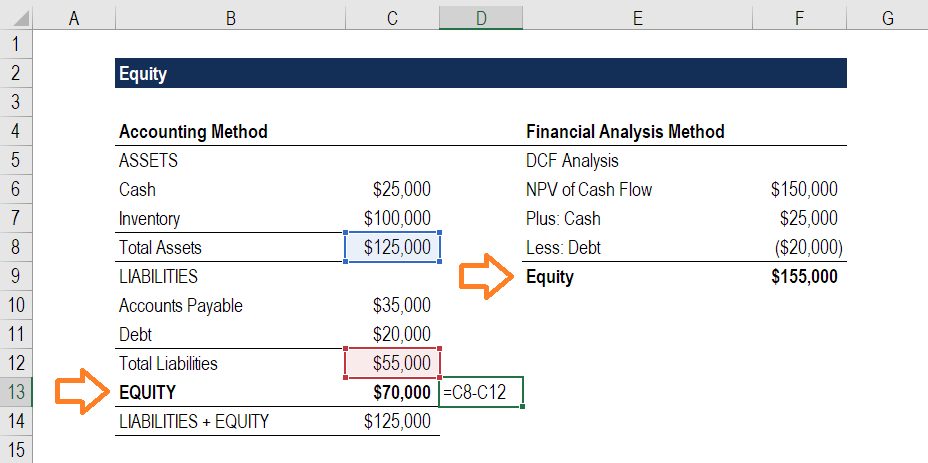

Let’s look at an example of two different approaches in Excel. The first is the accounting approach, which determines the book value, and the second is the finance approach, which estimates the market value.

Enter your name and email in the form below and download the free template now!

As you can see, the first method takes the difference between the assets and liabilities on the balance sheet and arrives at a value of $70,000. In the second method, an analyst builds a DCF model and calculates the net present value (NPV) of the free cash flow to the firm (FCFF) as being $150,000. This gives us the enterprise value of the firm (EV), which has cash added to it and debt deducted from it to arrive at the equity value of $155,000.

It is very common for this market approach to produce a higher value than the book value.

Thank you for reading CFI’s guide to Equity. To keep advancing your career, the additional CFI resources below will be useful: